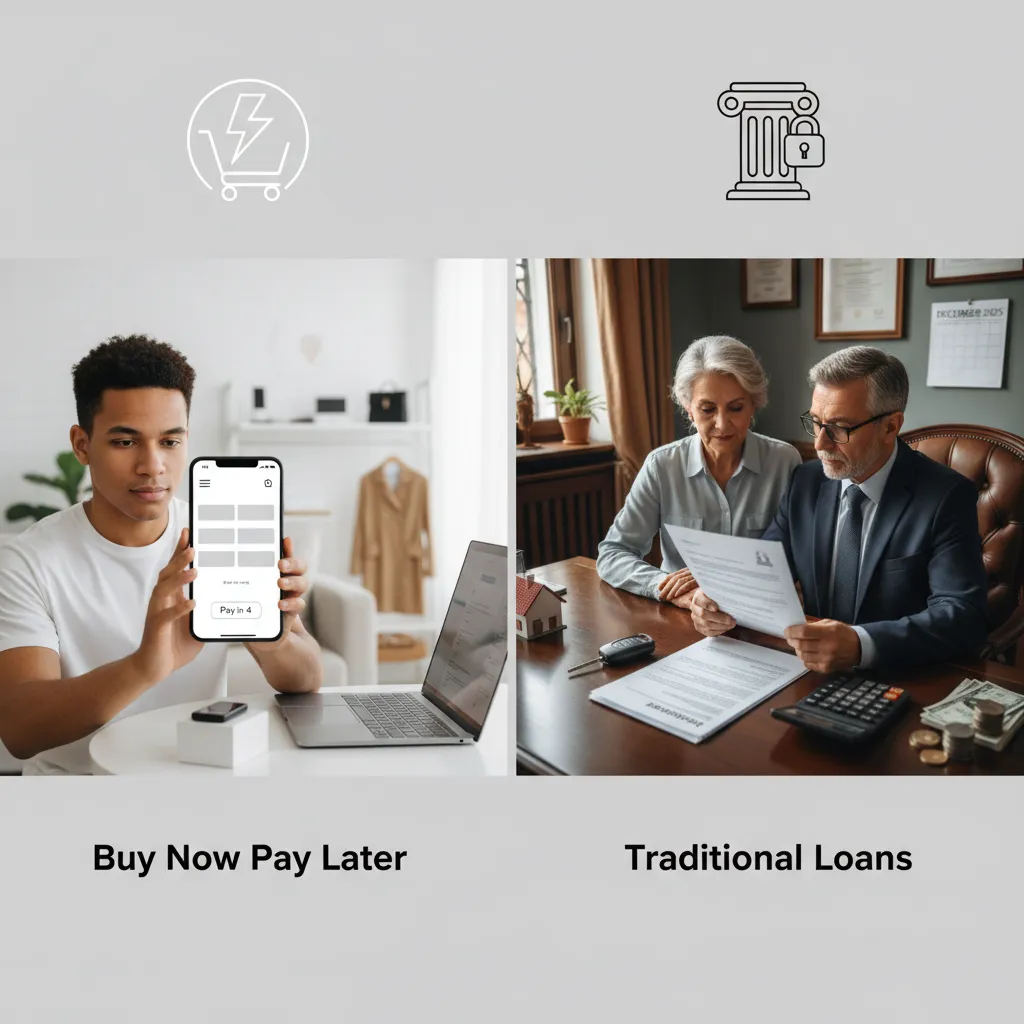

Buy Now Pay Later Services vs Traditional Loans: A Complete Comparison

In today’s rapidly evolving financial landscape, consumers are constantly looking for flexible payment options that suit their lifestyle and financial goals. Two of the most popular choices are Buy Now Pay Later services and traditional loans. While both provide a way to access products or services without immediate full payment, they differ significantly in structure, requirements, risks, and long-term impact. This article explores the differences between these two financial tools in depth to help you make informed decisions when choosing between them.

Understanding Buy Now Pay Later (BNPL) Services

Buy Now Pay Later services allow consumers to purchase products immediately and defer payment over a short period, usually in equal installments. Unlike traditional loans, BNPL does not always involve strict credit checks, making it appealing to younger shoppers and those with limited credit history.

Companies like Afterpay, Klarna, and Affirm have popularized BNPL by integrating directly with online stores, making the checkout process quick and seamless. The main selling point is convenience, but it comes with financial implications that consumers should understand.

Key Features of BNPL

- Quick approval with minimal requirements

- Short-term repayment structure (often 4–6 weeks)

- No or low interest if payments are made on time

- Integrated directly at the point of sale (online or offline)

What Are Traditional Loans?

Traditional loans are financial products offered by banks, credit unions, and other financial institutions. They provide borrowers with a lump sum of money that must be repaid over a fixed term with interest. These loans can be personal loans, auto loans, or even credit card balances.

Unlike BNPL, loans involve a more detailed application process, including credit checks, proof of income, and often collateral (for secured loans). They are designed for larger expenses and longer repayment periods.

Key Features of Traditional Loans

- Detailed application and approval process

- Repayment terms ranging from months to years

- Interest rates based on creditworthiness

- Used for major expenses like cars, education, or debt consolidation

BNPL vs Traditional Loans: A Historical Context

The rise of Buy Now Pay Later services began around the 2010s, fueled by e-commerce growth and consumer demand for instant solutions. They represent a new-age alternative to credit cards, especially for millennials and Gen Z.

On the other hand, traditional loans have existed for centuries as the backbone of global financial systems. They evolved alongside banking institutions and remain critical for large-scale financing, mortgages, and long-term credit building.

Why History Matters

Understanding the historical roots helps consumers recognize how BNPL fills gaps that traditional loans could not. While loans served major purchases, BNPL targeted everyday shopping needs, making credit more accessible at a micro-level.

Eligibility and Approval Process

One of the most significant differences between BNPL services and traditional loans lies in the approval process. BNPL providers often conduct soft credit checks or none at all, meaning approval is instant. This accessibility makes it attractive for people with limited or poor credit histories.

Conversely, traditional loans involve a more rigorous process. Lenders require credit reports, proof of stable income, debt-to-income ratios, and sometimes collateral. This ensures the borrower has the financial capacity to repay the loan but also excludes those with weak financial profiles.

Comparison Snapshot

- BNPL: Instant approval, minimal requirements

- Loans: Lengthy approval, higher requirements

Repayment Structures and Terms

BNPL repayment is structured into short-term, interest-free installments, typically over 4–6 weeks. If payments are missed, late fees or penalties may apply, but interest is generally avoided if consumers pay on time.

Loan repayment, on the other hand, is long-term and comes with fixed or variable interest rates. Payments are spread over months or years, making them suitable for financing larger purchases but also increasing long-term financial obligations.

Example:

Buying a $500 gadget with BNPL might mean four payments of $125, while a personal loan for the same amount could stretch over 12 months with interest, making the total cost higher.

Interest Rates and Fees

The cost of borrowing is another critical factor when comparing Buy Now Pay Later services vs traditional loans. BNPL services advertise zero-interest installments, which is true if payments are made on time. However, late payments can lead to high fees or even collections.

Traditional loans almost always involve interest, which can range from single digits to high double digits depending on creditworthiness and loan type. Additionally, loans may include processing fees, origination fees, or early repayment penalties.

Hidden Costs

- BNPL: Late fees, potential impact on credit score

- Loans: Interest accumulation, fees for processing or prepayment

Impact on Credit Scores

Credit history plays a crucial role in financial health. Most BNPL services do not initially report payments to credit bureaus, meaning timely payments may not build credit history. However, missed payments can be reported and negatively affect your credit score.

Traditional loans are directly tied to credit reporting. Timely repayments help build a strong credit profile, while defaults significantly harm it. For consumers looking to improve their creditworthiness, loans may be more beneficial in the long run.

Pro Tip: If building credit is a long-term goal, traditional loans or secured credit cards may serve better than BNPL services.

Financial Risks and Consumer Behavior

BNPL services are often criticized for encouraging impulse spending since approval is instant and repayment appears manageable. This can lead to consumers juggling multiple BNPL plans across different retailers, resulting in debt accumulation.

Loans generally require more planning and commitment, which reduces impulsive borrowing. However, the long-term financial obligations can strain budgets, especially if interest rates are high or income is unstable.

Behavioral Patterns

- BNPL: Encourages quick decisions, small-ticket purchases

- Loans: Encourages planning, larger purchases

Use Cases: When to Choose BNPL or Traditional Loans

Choosing between Buy Now Pay Later services and traditional loans depends on the context of your financial needs.

Best Situations for BNPL

- Small purchases like gadgets, fashion, or household items

- Consumers without established credit history

- Short-term financial gaps

Best Situations for Loans

- Major expenses like cars, medical bills, or home improvements

- Debt consolidation with fixed repayment terms

- Borrowers looking to build or improve credit scores

Future of BNPL vs Traditional Loans

The financial industry is evolving, and the line between BNPL services and traditional loans is beginning to blur. Many banks are introducing their own BNPL-like services, while BNPL providers are expanding into larger loan products.

Regulatory scrutiny is also increasing, especially for BNPL, to protect consumers from hidden debt risks. Traditional loans remain relevant, but the convenience of BNPL ensures it will continue to grow, particularly in the e-commerce sector.

Conclusion

Both Buy Now Pay Later services and traditional loans offer unique advantages and disadvantages. BNPL provides quick, interest-free access to small-ticket purchases but carries the risk of overspending. Traditional loans, though more complex and costly, are reliable for large expenses and credit building. The best choice depends on your financial goals, spending habits, and long-term plans.

Ultimately, responsible borrowing - whether through BNPL or loans - ensures financial stability and prevents debt traps. By understanding the differences, you can align your borrowing choices with your overall financial health.